Understanding Long-Term Care Tax Deductions

[vc_row][vc_column][vc_column_text]With the tax filing deadline just over one month away, it’s important to understand the tax benefits that come with obtaining long-term care insurance policies. In 2016, the Internal Revenue Service (IRS) increased the amount that taxpayers can deduct from their 2016 taxes as a result of buying long-term care insurance.

Premiums for “qualified” long-term care insurance policies are tax deductible to the extent that they, along with other unreimbursed medical expenses (including Medicare premiums), exceed 10 percent of the insured’s adjusted gross income, or 7.5 percent for taxpayers 65 and older (through 2016).

These premiums — what the policyholder pays the insurance company to keep the policy in force — are deductible for the taxpayer, his or her spouse and other dependents. (If you are self-employed, the tax-deductibility rules are a little different: You can take the amount of the premium as a deduction as long as you made a net profit; your medical expenses do not have to exceed a certain percentage of your income.)

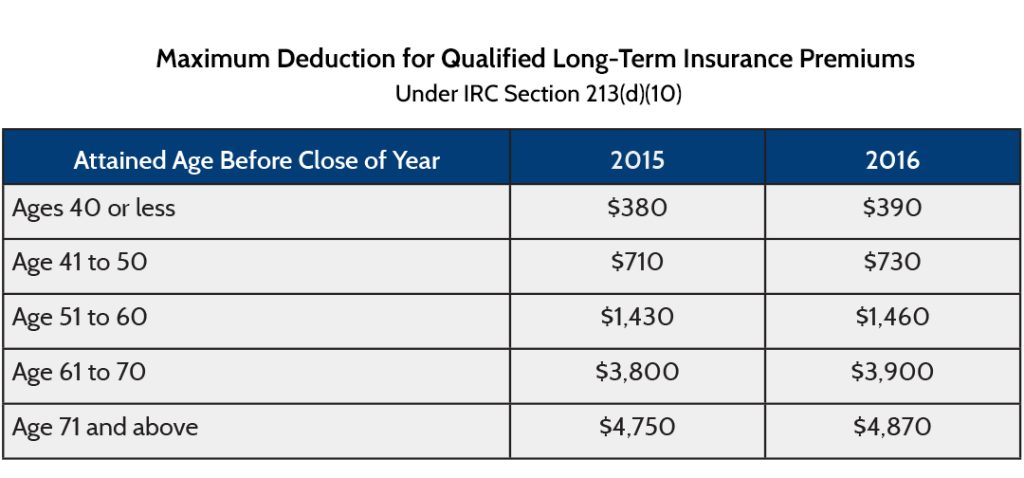

However, there is a limit on how large a premium can be deducted, depending on the age of the taxpayer at the end of the year. Following are the deductibility limits for 2016. Any premium amounts for the year above these limits are not considered to be a medical expense.

Another change announced by the IRS involves benefits from per-diem or indemnity policies, which pay a predetermined amount each day. These benefits are not included in income except amounts that exceed the beneficiary’s total qualified long-term care expenses or $340 per day, whichever is greater.

For these and other inflation adjustments from the IRS, click here.

What Is a “Qualified” Policy?

To be “qualified” policies issued on or after January 1, 1997, they must adhere to certain requirements: the policy must offer the consumer the options of “inflation” and “non-forfeiture” protection, although the consumer can choose not to purchase these features. Policies purchased prior to January 1, 1997, will be grandfathered in and treated as “qualified” policies as long as they have been approved by the insurance commissioner of the state in which they are sold.

[/vc_column_text][/vc_column][/vc_row]

Recent News

A Social Experiment | What Are The Chances?

The potential need for long term care is a topic most people would rather avoid. But not talking about it doesn’t make the issue go away. It only delays planning and leads to potential confusion and financial impact for not just those who may need care, but their family and friends. The reality is that … Continue reading "A Social Experiment | What Are The Chances?"

November Is Long-Term Care Awareness Month!

Have you planned ahead to secure your financial future? In today’s world, home is more important than ever. It’s the one place we all feel safe and secure. November is National Long-Term Care Awareness Month, an event recognized by Congress and a number of states, designated to educate Americans on the growing need for long-term … Continue reading "November Is Long-Term Care Awareness Month!"

Another Inflation Stress: Rising Costs of Senior-Living Homes Strain Families

Inflation is fueling cost increases at nursing homes and assisted-living and independent-living facilities, which is tough for seniors on fixed incomes Eldercare facilities are raising prices and adding new fees, straining older Americans and their families who step in to help. Dan Gallo recently received a letter saying a new inflation-related daily fee of $25 … Continue reading "Another Inflation Stress: Rising Costs of Senior-Living Homes Strain Families"

Updated: NAIC Shopper’s Guide to Long-Term Care

The National Association of Insurance Commissioners (NAIC) has updated their consumer publication, A Shopper’s Guide to Long-Term Care Insurance. The NAIC wrote this Shopper’s Guide to help you understand long-term care and the insurance options that can help you pay for long-term care services. The decision to buy long-term care insurance is very important. You … Continue reading "Updated: NAIC Shopper’s Guide to Long-Term Care"